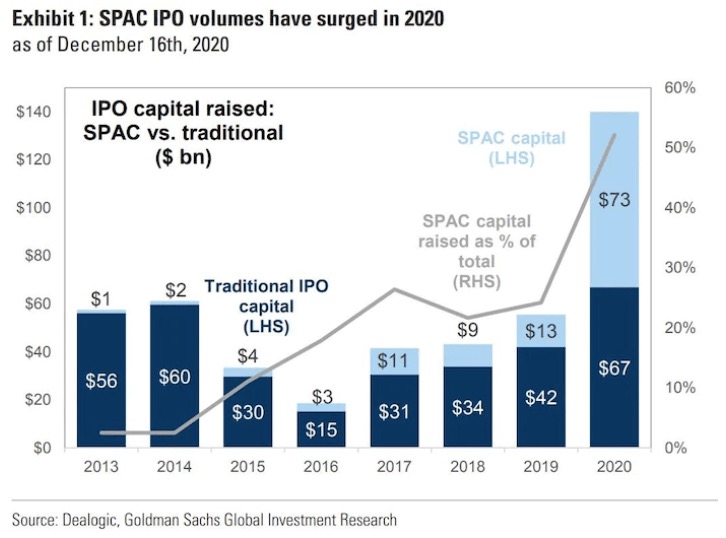

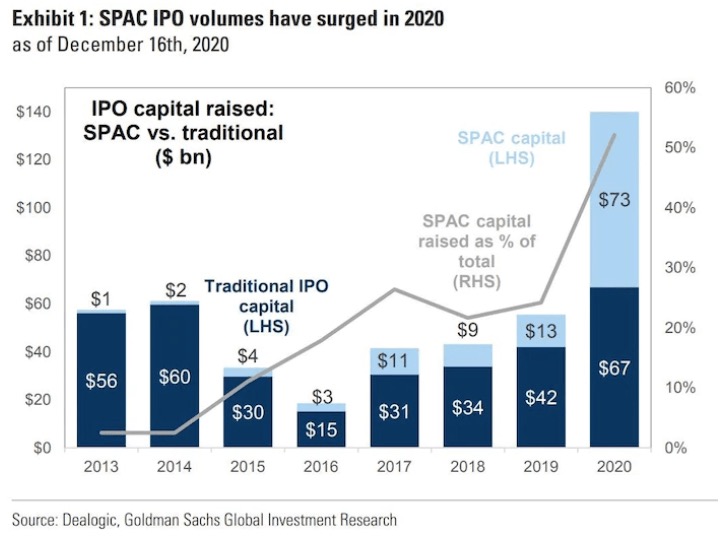

CBS MarketWatch declared 2020: The Year of the SPAC (Special Purpose Acquisition Corporation). A record 219 companies went public through this fundraising vehicle that uses a reverse merger with an existing private business to create a publicly-listed entity. This accounted for more than $73 billion dollars of investment, providing private equity startups a new outlet to raise capital and provide shareholder liquidity. According to Goldman Sachs, the current trend represents a “year-over-year jump of 462% and outpacing traditional IPOs by $6 billion.” In response to the interest in SPACs, the Securities and Exchange Commission agreed recently to allow private companies to raise capital through direct listings, providing even more access to the public markets outside of Wall Street’s traditional institutional gatekeepers.

For the past few months, the SPAC craze has spilled over to the robot and remote sensing industries. SoftBank announced it is raising $525 million in a blind pool SPAC for investments in artificial intelligence. In the filing with the SEC, Softbank states, “For the past 40 years, SoftBank has invested ahead of major technology shifts. Now, we believe the AI revolution has arrived.” In 2017, SoftBank’s Chief Executive, Masayoshi Son (nicknamed Masa) predicted that by 2047, robots will outnumber humans on the planet with 10 billion small humanoids (like its own Pepper robot) rolling the streets. An outspoken believer in Singularity, Masa has not been shy about investing in the robotics sector with ownership stakes in Whiz, Pepper, Bear, and Brain Corp. The company sold its interests in Boston Dynamics to Hyundai for a billion dollars earlier this month. When launching his own venture capital fund in 2018, Masa declared, “I am devoting 97% of my time and brain on AI.” This past month, Masa’s $100 billion Vision Fund had a huge portfolio win with the IPO of DoorDash, erasing earlier losses of failed investments in WeWork and OneWeb. In that spirit, it is not surprising that the SPAC filing exclaims: “COVID-19 has pulled this future-forward by dramatically accelerating the adoption of digital services. During this time, we intersected with many compelling companies that wanted our support at IPO and beyond, but we lacked the vehicle to partner with them. This trend has only increased over the past year as more companies have decided to list publicly.”

SoftBank’s optimism is further validated by the success of SPACs in acquiring hardware sensor companies. In December, Ouster became the fifth LiDAR startup to go public through a SPAC this year. Already trading on the markets is Velodyne, Luminar, Innoviz, and Aeva. Each of these companies raised hundreds of millions of dollars at valuations exceeding a billion dollars. Some have fared well in the public markets, such as Luminar doubling its valuation in a few weeks. Others, like Velodyne, have had more difficulty. Velodyne’s shares fell by half since its listing in September (it is currently trading modestly above its initial price). As hardware is tough, staying private comes at the cost of founder dilution and overvaluation. SPACs offer startups and their investors quicker access to capital and greater liquidity, enabling investors to reinvest their returns in the autonomous sector and ultimately driving innovation in advance of greater adoption.

Recently, I caught up with Andrew Flett, General Partner of Mobility Impact Partners, who raised $115 million for a new SPAC – Motion Acquisition Corp. (ticker symbol MOTNU). Flett’s investment vehicle is still on the hunt for an acquisition of “target businesses in connected vehicle industries globally, which include companies providing transportation software and cloud solutions for fleet management, freight and logistics, and mobile asset management applications.” When speaking with Flett, he described his inaugural experience in the space as follows, “This is the first SPAC I have been directly involved with but the mechanism has evolved and matured over the last couple of decades. They are popular now as a function of the same yield scarcity and immense liquidity that has been driving public equity speculation. There will be both highly speculative companies and companies with solid fundamentals in any wave of interest. This wave is no different.” He astutely points to previous SPAC upticks (since the 1980s) led by dubious underwriters that used the mechanism as a way to make a quick buck through “pump-and-dump” schemes. These market manipulators, many still serving jail time, quickly promoted stocks on the exchanges to only rapidly sell their own interests in the companies before other investors were legally able to trade the shares, ultimately devastating the startup’s and its shareholders’ values. This is compounded by the increased expenses and transparency of publicly traded listings, leaving startup founders ill-prepared for their new role on the NASDAQ or NYSE.

Unlike the past, many of the newly formed SPACs have been managed by brand name investors such as Richard Branson (Virgin Galactic), Bill Ackman (Pershing Square) and Peter Thiel (Bridgetown). The performance of the newly listed SPAC 2020 crop has been very impressive, outpacing the S&P, with Draft Kings and Nikola leading the charge with triple-digit returns. In nudging Flett for his opinion of these managers, he cautions, “Smart guys. Is it just a branding exercise or will they be involved in the asset evaluation and ultimate de-SPACed company? In the end, the asset needs to stand on its own and regardless of how it gets there (IPO, Direct Listing, SPAC), once public it is a pure apples-to-apples performance comparison dependent on strategy, management, and execution. If the public company does not benefit from their wisdom, it does not matter what brand is attached at the front end.”

Flett advises founders not to be too easily seduced by public capital, rather “focus on your company. If your company cannot absorb the responsibilities and overhead of being a public company, it is not the right option for you.” Gauging his view of Softbank’s latest announcement, “Like most Private Equity or institutional investors, it is simply a cash grab and an alternative vehicle to demonstrate their investing acumen. I prefer seeing Softbank doing reasonably sized SPACs than raising another misguided Vision Fund,” Flett optimistically opines. However, at the end of the day, the SPAC pioneer reminds us that the market is cyclical and the window of opportunity will eventually close, “As some of the speculative bets burn investors and yield alternatives appear, the SPAC market will slow.”