This past week’s historic eclipse could be an analogy for the future of automation. The all powerful human is being shadowed by the subservient autonomous machine. Like the moon’s dependency on the sun, robots could not exist without mankind. As we reached total darkness, one was tempted to be like Icarus, while in reality our naked eyes would have burned with blindness. We have already seen fatalities with mortals trusting their wax wings too much, in the form of auto-pilot crashes and industrial accidents. The brightness of the sun returned after a few minutes, leaving in its shadow a reminder that the future arrives with great promise and fragility.

Last month, while speaking at the National Governors Association Summer Meeting, Elon Musk exclaimed that artificial intelligence (AI) is the “biggest risk we face as a civilization.” He explained that “AI is a rare case where I think we need to be proactive in regulation instead of reactive. Because I think by the time we are reactive in AI regulation, it’s too late.” He then illustrated his point with a famous Hollywood-like image, “Until people see robots going down the street killing people, they don’t know how to react because it seems so ethereal.”

Musk’s view is echoed by Nobel Prize Professor Stephen Hawking who has previously said: “Alongside the benefits, AI will also bring dangers, like powerful autonomous weapons, or new ways for the few to oppress the many. It will bring great disruption to our economy.”

The dissenters of Musk and Hawking have included Mark Zuckerberg and numerous academics; however, few have questioned the need for a frank discussion on AI. Even Arizona State University computer scientist Subbarao Kambhampati acknowledged that “there needs to be an open discussion about the societal impacts of AI technology,” while, at the same time, criticizing Musk’s sensational example.

As I write this article, the stock market soars to record highs even though it is one of the most highly-regulated industries in America. One of the largest areas of transformative growth in AI is happening today in the financial services sector. According to PWC, by 2020 more than 20% of the established “too big to fail banks” are at risk for disruption. The perfect storm hovers over one of the world’s largest businesses with the confluence of mobile technologies, cloud-computing, blockchain, and robo-advisors. As CTO’s look to transform their enterprises, hiring a Chief Robotics Officer will no longer be a luxury afforded by the most innovative, rather it will be a requirement to thrive in the new autonomous economy.

Earlier this summer the World Economic Forum (WEF) warned banks that their competition might not be other institutions but tech companies looking to expand their relevance for the growing millennial economic demographic. The report highlighted that many financial institutions are turning to Amazon, Google and Facebook instead of building technology in house. Already, Amazon Web Services (AWS) counts such notable firms as Aon, Capital One and Nasdaq as customers.

Rob Galaski of Deloitte, who co-authored the report said, “Fintechs now define the tempo and direction of innovation in financial services, but high customer switching costs and the rapid response of incumbents [established banks] has challenged their ability to scale. The ability to be a fast follower has proven more important than being first for large financial institutions. Agile incumbents have used the fintech ecosystem as a supermarket for capabilities, making the ability to nurture and rapidly form partnerships a critical ingredient to banks’ competitive success.”

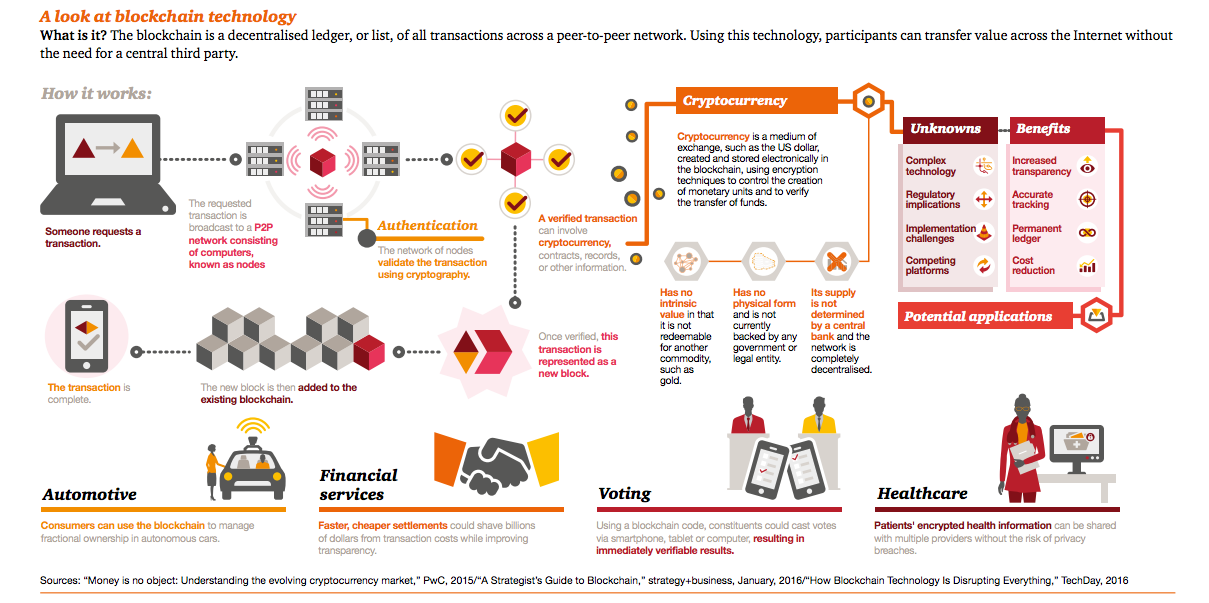

In addition to cloud computing, blockchain has been a particular interest to high finance, especially to replace human-run clearing houses with instantaneous automated ledgers. Following the adage that ‘no one gets fired for hiring IBM,’ Brigid McDermott of IBM boasts, “Some of the start-ups that are coming in don’t necessarily understand the scope of the transactions that are running all the time, and when you think about banking as an $8-9 trillion industry – that’s a lot of transactions. When you come at it as a start-up and you’re trying to look at a small part, do you really have a sense of what the transformation is that needs to happen?”

McDermott’s words are reminiscent of the famous quote by Jim Keyes, CEO of Blockbuster in 2008, who declared that “Neither RedBox nor Netflix are even on the radar screen in terms of competition.” IBM would be foolish to think it has already cornered the blockchain market, since in its rearview mirror are thousands of startups that have collectively raised over $30 billion in the past three years. One of the most notable private financings this summer was a $100 million round in R3, a consortium of 80 financial institutions to advance blockchain’s distributed ledger technology – enabling contracts and automated secure transaction clearing. R3’s financing was led by Intel, Bank of America, and Wells Fargo to bolster the development of its open-source platform called Corda that is also part of the Hyperledger Foundation (a blockchain division of the Linux Foundation).

David Rutter, CEO of R3, stated that his vision for Corda is to become the de facto standard for financial transactions. “We are on our way to becoming the new operating system for financial services,” said Rutter. R3 already competes with J.P. Morgan’s Quorum, IBM’s Fabric, Intel’s Sawtooth Lake and startups Ripple, Chain, and Digital Asset Holdings. In R3’s favor is a long investor roster that reads like the who’s who of Wall Street. Blockchain’s ledger technology will become a critical component of the future of other aspects of the the autonomy economy from self-driving cars to healthcare to even securing voting booths.

Automating the back office is only the first step to utilizing data-driven technologies across global banking. AI is being deployed in client-led initiatives as well, including: credit scoring, lending applications, chat bots, mobile assistants, algorithmic trading, market research, debt collection, predictive analytics, and compliance systems. Ophir Gottlieb, co-founder of Capital Market Laboratories, explains that today’s technology is the culmination of three waves that started in the 1990s with the Internet and this past decade with big data. Gottlieb states that “the third wave will be the consumption of this data and the transformation of it into knowledge. This echoes the same transformation in technology turning big data into knowledge using machine learning broadly and AI specifically.”

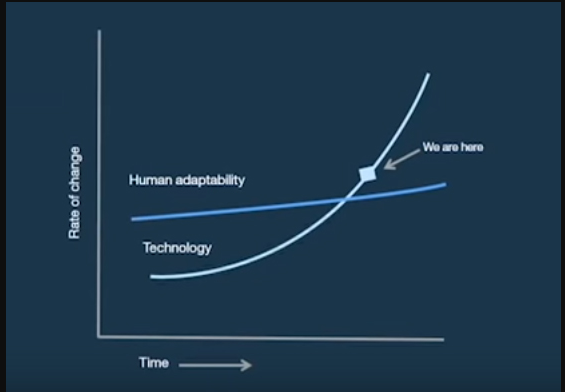

Musk’s fear is real; technology is accelerating faster than mankind’s ability to adapt. Even human-intensive businesses like fixed income and wealth management are turning to high-frequency trading algorithms instead of physical traders. New York’s Stock Exchange has become a backdrop to financial television shows, a mere shadow of the heralded marketplace it was only a decade ago. Mark Watters, director of electronic trading provider AxeTrading, summed it best, “Most people are moving towards artificial intelligence or algorithmic analysis of the data to draw these insights automatically.”

So as we bask in the remaining days of August, the future of deep learning systems doesn’t wait for humans to return to their factory floors and corner offices. While our creative spark is still required to guide the implementation of intelligent machines, this is only temporary. Or is it, I mean who else could think of robotic short-order cooks?